Contrary to popular belief, the options for senior living accommodations are as diverse as the thousands of people who call them home. Your unique needs are different than those of your neighbor’s. It’s important to do your research and find a place that not only fits your requirements for health and safety, but feels like home as well.

There are some similarities between senior living options but there are a lot of differences too. For example, if you just want to move to a place where you feel more supported and forge connections with neighbors, a senior living community is probably a good fit. Or, if you are dealing with a loved one’s symptoms of dementia or a diagnosis of Alzheimer’s disease, you may want to look into a memory care option that can offer the best resources possible for the health of their mind.

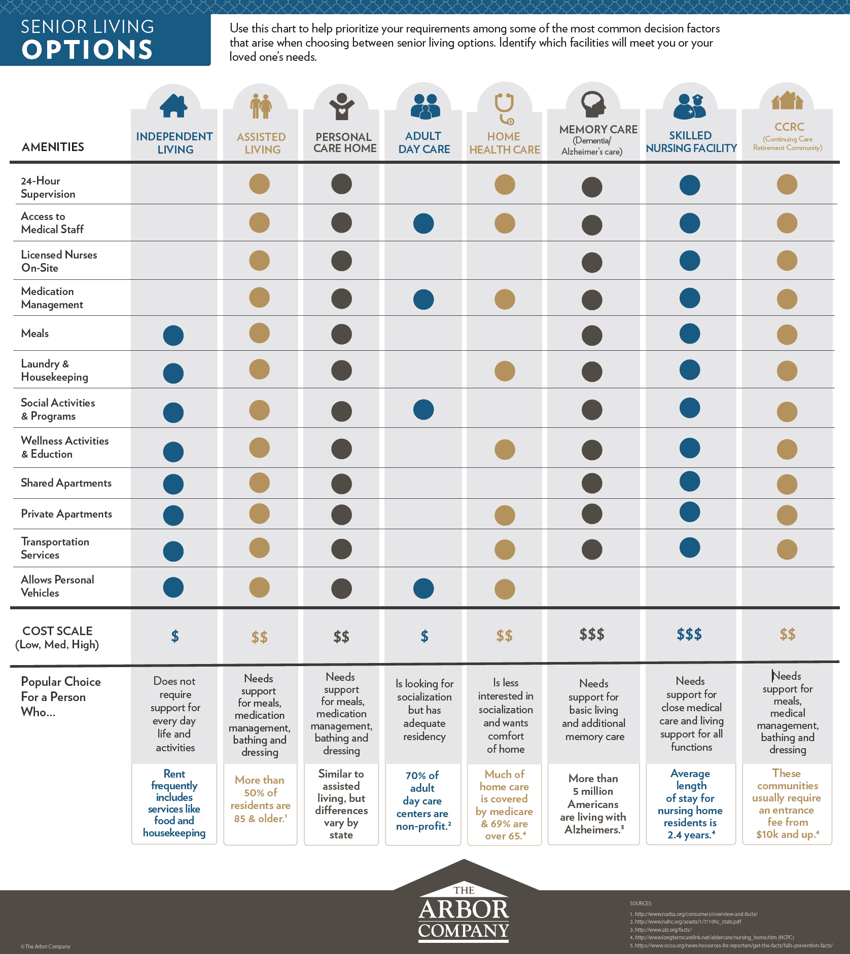

The point is, there is a lot to consider and there are a lot of options to choose from. We’ve put together this infographic with some of the most common decision factors to help walk you through these choices. Now keep in mind, this information is a great start but there is a lot more that goes into choosing a senior living facility than a few bullet points on a checklist. We’d love to talk to you and answer any questions that you may have — just select the “contact us” button at the top of the page. We’re here to help!